What is a Charitable Remainder Trust (CRT)?

It is a trust where non-charitable beneficiaries (usually the grantor and grantor’s spouse) receive payments at least annually during their lives or for a number of years, and a charity receives the trust assets remaining

at the end of the trust term.

A charitable trust is also referred to as a “split interest trust”. This is because the beneficial interests in the trust are “split” between the initial non-charitable beneficiaries and the charitable beneficiaries that receive what remains at the end of the trust term. We will refer to the initial noncharitable beneficiaries as the “Lead Beneficiaries”.

When does it make sense to have a CRT?

CRTs should be considered when a charitably inclined individual wants to diversify a highly appreciated portfolio, while generating cash flow and an immediate income tax deduction. An individual may want to sell an appreciated concentrated stock position but may be deterred by the capital gains tax consequences. Transferring those assets to a CRT – and then diversifying inside the CRT – is a possible solution. Doing so will not avoid income tax (as explained below), but it will provide for income tax deferral over the life of the CRT.

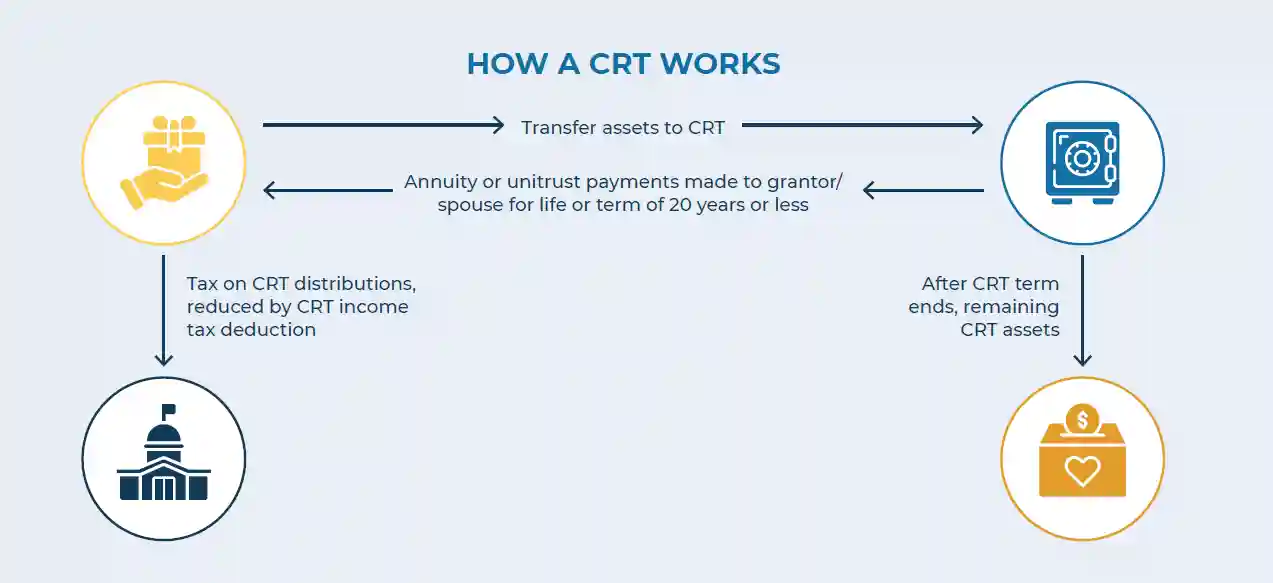

How does a CRT work?

The grantor initially funds the CRT with highly appreciated assets. When the CRT sells the highly appreciated assets, the CRT itself is not subject to capital gains tax, thus preserving the full value of the appreciated assets to reinvest in a diversified portfolio. The capital gains taxes will be spread out and payable as the Lead Beneficiaries receive payments from the CRT. In addition, the grantor receives an immediate income tax deduction.

Is income tax imposed on the distributions and who pays it?

CRTs are exempt from income tax. The CRT assumes the grantor’s adjusted cost basis and holding period in the property. If the CRT sells appreciated property, neither the grantor nor the CRT will pay immediate income tax on the sales.

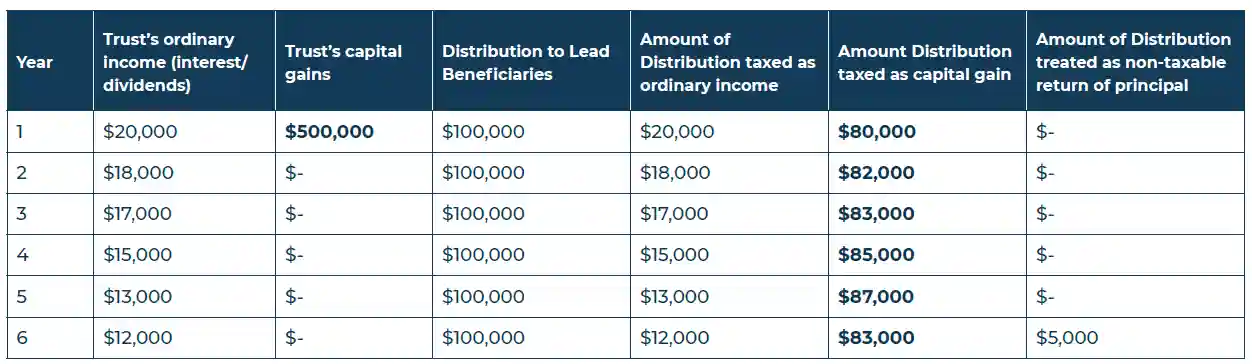

However, when the Lead Beneficiaries receive payments (at least annually), those payments are subject to income tax. The following rules show how these payments are taxed, and the chart below is an illustration of these rules in effect:

- First, the payment is taxed as ordinary income to the extent of the CRT’s ordinary income for that year and undistributed ordinary income from prior years.

- Second, the distribution is treated as capital gains to the extent of the CRT’s capital gains for that year and undistributed capital gains from prior years.

- Third, the distribution is treated as other income to the extent of the CRT’s other income for that year and undistributed other income from prior years.

- Distribution amounts in excess of the above items of income are treated as non-taxable return of principal.

As you can see from the chart below, even though $500,000 in capital gains were incurred in year 1, the tax on that gain is not immediately payable but is instead spread out over a 6-year span as the distributions are paid out.

How long can the CRT last?

A CRT may last for the Lead Beneficiaries’ joint lives or for a term of years (the term may not exceed 20 years). In addition, the actuarial value of the CRT remainder left to charity must be least 10% of the initial CRT value, determined at time of funding. This “10% test” creates a floor as to how young the Lead Beneficiaries can be. If the Lead Beneficiaries are too young, the CRT will fail the 10% test. The “10% test” depends on three factors:

- The term of the CRT or for lifetime CRT’s, the Lead Beneficiaries’ life expectancies,

- The payment amount each year, and

- The IRC 7520 rate (defined as 120% of the federal midterm interest rate).

How often are distributions made?

Distributions are typically made annually or quarterly but can be weekly, monthly or semi-annually as well.

How are the distributions amounts determined?

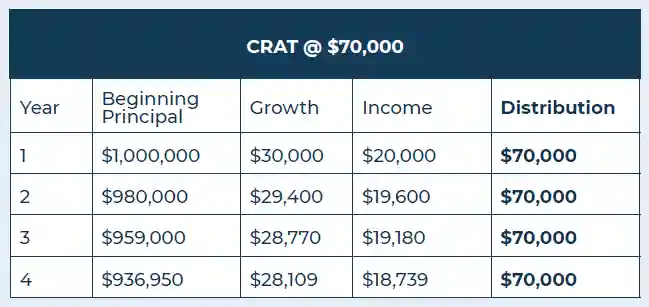

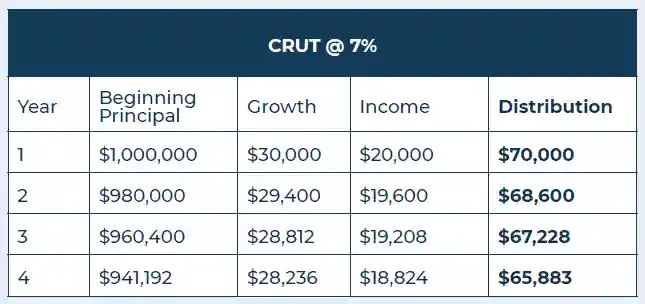

The IRS rules require the amount be at least 5% but no more than 50% of the trust assets. The maximum distribution amount depends on the length of the CRT term or for lifetime CRTs, the Lead Beneficiaries’ life expectancies. The distribution schedule and amounts also depend on the type of CRT being used. The following tables illustrate this (all illustrations assume 3% growth and 2% income, so overall rate of return of 5%):

A Charitable Remainder Annuity Trust (CRAT) pays out the same dollar amount each year, so the Lead Beneficiaries will receive the same amount no matter if the trust value increases or decreases.

A Charitable Remainder Unitrust (CRUT) pays out a fixed percentage of the trust value each year. The amount will be recalculated each year, and the Lead Beneficiaries receive larger payments that year if the CRUT’s rate of return exceeds the fixed percentage payout, and smaller payments that year if the CRUT’s rate of return is less than the fixed percentage payout.

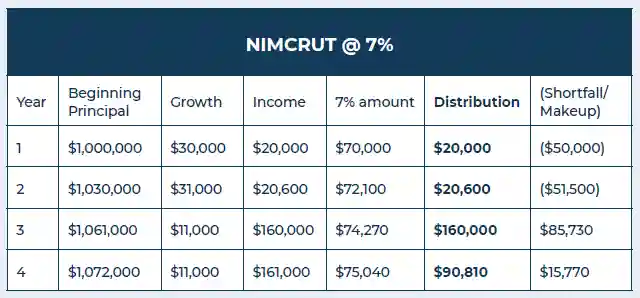

A Net Income with Makeup CRUT (NIMCRUT) pays the Lead Beneficiaries the lesser of the net income or the fixed percentage each year. If the NIMCRUT income falls below the fixed percentage payout in certain years, payments can be made up in future years if net income exceeds the fixed percentage. A NIMCRUT may appeal to charitable individuals with illiquid assets (i.e., artwork, collectibles), and no current cash needs. While the NIMCRUT holds the illiquid assets, there will be little to no income distributed to the Lead Beneficiaries but when the illiquid asset is sold, there could be more than enough to make up for those shortfall years. Below, the $101,500 shortfall total in years 1 and 2 is made up in years 3 and 4, when net income (i.e., the gain from a sale of some of the collectibles allocated to income) exceeds the fixed percentage amount.

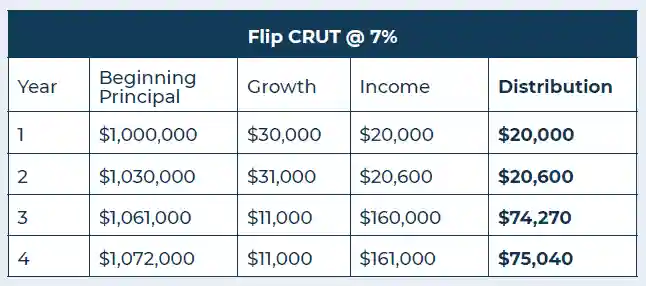

A Flip CRUT works in certain situations where no current cash flow need exists, but the occurrence of a specific definable future event would trigger a cash flow need. A Flip CRUT changes from a NIMCRUT to a normal CRUT when a specified event occurs. For example, the NIMCRUT could flip to a regular CRUT when grantor reaches a certain age (i.e., anticipated retirement age 2 years from now) or when a grantor’s pension terminates (at grantor’s passing). In that scenario, flipping to a normal CRUT in year 3 provides the Lead Beneficiaries with a guaranteed payment stream to offset the income loss resulting from the anticipated retirement or terminated pension.

Do I get a charitable deduction?

Yes, the grantor receives an immediate income tax deduction equal to the present value of the projected remainder interest that passes to the charity. The available charitable income tax deduction is limited to 60% of adjusted gross income (AGI) for the year if cash is gifted to the CRT with a public charity or donor advised fund as the charitable remainder beneficiary. However, the deduction may be limited to 30% or 20% of AGI for the year, depending on the type of property you give to the CRT (short-term v. long-term capital gain property) or the type of charitable organization named as remainder beneficiary (church/school/public charities/donor advised funds v. family private foundations). The good news is that you may carry over any unused charitable deduction amount from any year in which the remaining deduction surpasses these limits, up to five years.

Are there restrictions on what charity can be named as remainder beneficiary? Can I change the charitable beneficiary during my life?

Yes, the charitable remainder beneficiary must be an organization described in Internal Revenue Code Section 170(c), such as a public charity, donor advised fund, religious organization or a private foundation. You may change the charitable beneficiary during your life, but it is best to give an independent trustee this power to avoid risk of the CRT being included in your taxable estate. For clients who think they may change the charitable beneficiary in the future, donor advised funds can be named as the charitable

beneficiary, as the charities in the donor advised fund can be changed at any time without the need for an independent trustee.

Can my private foundation be the remainder beneficiary?

Your private foundation can be the remainder beneficiary, but the income tax deduction will usually be less. The CRT may also be subject to investment limitations that would not apply if a public charity or donor advised fund were the remainder beneficiary.

Who can be the trustees?

Often, grantors will name themselves or their spouses as trustee. The grantor’s other family members may also act as trustees. An independent trustee may be needed if CRT holds unmarketable or hard to value assets such as closely held stock or artwork, or if the grantor thinks he may want to change the charitable beneficiary later.

Do I have to pay gift tax when I set up a CRT?

Generally, no. However, if someone other than grantor or his spouse receives the payments, then the grantor has made a taxable gift to that someone equal to the present value of the annuity or unitrust amounts paid to that person over the trust term, calculated when the CRT is created. The grantor may use his or her available unified credit to offset gift tax due on the amount passing to Lead Beneficiaries other than himself or his spouse. The remainder passing to the charities is always gift tax free because of the charitable deduction.

Is the CRT includible in my estate?

Generally, by gifting assets to a CRT, a grantor removes those assets from his taxable estate. The remainder passing to the charities is not includible in the grantor’s taxable estate. There is no estate tax

consequence so long as the grantor and her spouse are the only Lead Beneficiaries.

However, in situations where someone else (i.e. the grantor’s children) is a Lead Beneficiary, there may be an estate tax consequence. This can happen when a grantor, concerned about her premature death, sets up her CRT so that her children receive the payments after she has passed away, with the grantor reserving the right to revoke the children’s payments in her Will. By reserving the right to revoke, the grantor avoids gift tax consequences, because the right to revoke causes the gift to be incomplete. However, if the grantor fails to revoke the children’s payments before her passing, the entire CRT would be includible in the grantor’s estate, reduced by an estate tax charitable deduction equal to the present value of the charitable remainder interest based on the fair market value of the CRT and the children’s life expectancies on the date of the grantor’s death.

Wealthspire Advisors LLC, Fiducient Advisors LLC, Wealthspire Retirement, LLC dba Wealthspire Retirement Advisory, and certain other affiliates are separately registered investment advisers. © 2024 Wealthspire Advisors

This material should not be construed as a recommendation, offer to sell, or solicitation of an offer to buy a particular security or investment strategy. The information provided is for informational purposes only and should not be relied upon for accounting, legal, or tax advice. While the information is deemed reliable, Wealthspire Advisors cannot guarantee its accuracy, completeness, or suitability for any purpose, and makes no warranties with regard to the results to be obtained from its use.

This material is provided for informational purposes only and was created to provide accurate and reliable information on the subjects covered. It should not be construed as a recommendation, offer to sell, or solicitation of an offer to buy a particular security or investment strategy, and should not be relied upon for accounting, legal, or tax advice. The services of an appropriate professional should be sought regarding your individual situation. You should not act or refrain from acting on the basis of this content alone without first seeking advice from your tax and/or legal advisors. While the material was prepared using public information and is deemed reliable, Wealthspire Advisors cannot guarantee its accuracy, completeness,

or suitability for any purpose, and makes no warranties with regard to the results to be obtained from its use.

Wealthspire Advisors and its representatives do not provide legal or tax advice, and Wealthspire Advisors does not act as law, accounting, or tax firm. Services provided by Wealthspire Advisors are not intended to replace any tax, legal or accounting advice from a tax/legal/accounting professional. Certain employees of Wealthspire Advisors may be certified public accountants or licensed to practice law. However, these employees do not provide tax, legal, or accounting services to any of clients of Wealthspire Advisors, and clients should be mindful that no attorney/client relationship is established with any of Wealthspire Advisors’ employees who are also licensed attorneys.