Recap

When we all look back at our quarterly notes written throughout 2022, there will be a common refrain. It is as though the finance world decided to take a page out of the music industry's book by recycling a melody with only slight variations. This is our third quarterly commentary this year, and we have also put out a few other market updates, yet all sound out three major chords – inflation, the Fed, and volatility (and basically in the same order).

Echoing past quarters, 2022 continues to be one of the worst starts for a balanced portfolio in modern history. U.S. Bonds are suffering one of their most difficult years since before Paul Volker (think 1979). With stocks down more than 20%, a conservative portfolio is not doing that much better than an aggressive one. This is not only a U.S. phenomenon. We see comparable and often more dire performance overseas in dollar terms. In short, this is an incredibly challenging environment for all investors that demands a level of patience that is hard to maintain in the face of constant headlines. Like we did during the 2016 sell-off, Brexit, U.S. elections, COVID-19, and other trying periods, we hope to provide context around why this is happening, emphasize the importance of avoiding knee-jerk reactions, and highlight potential opportunities ahead.

Why?

In our Q1 letter, we talked about the Fed and bonds. In Q2, we focused on inflation. In those, we covered how inflation got to this level, a sequence of: COVID-related manufacturing closures and supply-chain bottlenecks, trillions of stimuli looking for a place to go in an economy that is nearly 70% consumption, shrinking labor force participation and a corresponding growing need for workers (thus wage growth), low housing supply, continued zero COVID shutdowns in China, and eventually the war in Ukraine.

At the same time, the Fed dropped interest rates from around 1.5% to zero in March of 2020 and kept them there for almost two years despite inflation shooting up through much of 2021 (hitting 7% YoY in December 2021). As a reminder, the Fed has a somewhat convoluted mandate or purpose “to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.” The tagline in 2020 and 2021 was that inflation would be “transitory”. This proved to be true for the early offenders (rolling over lumber prices, shipping costs, used cars, etc.), but other “stickier” components eventually started to rise. Coming into the year, the Fed looked like it was losing inflation-fighting credibility. In fact, markets were pricing in just three 25 bps rate hikes for 2022 at the start of the year, which translated into the Fed Fund rate being below 1 by the end of this year.

As it turns out, the Fed does not like to lose credibility when it comes to inflation. A few very hawkish speeches and several 75 bps rate hikes later, market expectations now reflect 17 hikes for 2022. For context, each 25 bps (.25%) is considered one hike, thus when the Fed hiked 75 bps recently, it was deemed to have made three hikes. This would put the Fed Funds rate between 4.25% and 4.5% by year-end. That is a massive turn of face and translates into the most aggressive start to a Fed hiking cycle in over 40 years. It has resulted in yields rising not only on short-term bonds (which are tied to the Fed Funds rate), but also on longer term bonds. Rising rates directly translate to bond weakness (yields up, prices down) and also negatively impact many equities. Why? Rising rates raise the cost of borrowing for companies that need to borrow and raises the discount rates for cash flows for all. The longer the growth trajectory reflected in current pricing, the more pain. That may sound technical in nature, but simply look at how much house you can afford with a 15-year mortgage at 2% vs. 6% or a 30-year mortgage at 3% vs. 7%. Keeping monthly payments the same, you can afford roughly 26% less house with a 15-year mortgage and 36% less house for a 30-year mortgage. Said differently, rate punitiveness increases with time.

With all that discounted, markets may not be down in excess of 20% this year if there was a better understanding of where and when the Fed actually stops. Fear of the Fed is back. Martin Zweig’s famous line of “Don’t Fight the Fed” for so long supported liquidity and bullishness in the face of elevated valuations. Now it is showing its other meaning.

We can already see markets pricing in the Fed cutting interest rates in 2023-2024, but there has been a lot of variability in that assumption and nothing from the Fed to say that they will veer off the path. An overly aggressive Fed is often followed by a recession, the fear of which provides a more likely catalyst for why equities are down as much as they are this year.

Now What?

With that in mind, we are back in an environment where bad is good and good is bad. This was the refrain during the quantitative easing environment, when bad news translated into liquidity injections and therefore price support. Avoiding a fight with the Fed now means hoping for weaker economic data tied to inflation. That means reduced job openings, higher unemployment, falling housing prices, and overstocked inventories. Some of those are starting to happen without the Fed’s blunt tools (e.g., high inventories, 1.7 million housing units under construction, 890k of which are apartments – the highest ever). Others, like existing single-family home prices, have the Fed to thank directly for higher mortgage rates and lower affordability. Lost in the headlines but not lost for our clients and portfolios is the fact that higher rates are providing the best opportunity for savers in well over a decade. Cash yields top 2% today, and for the first time since late 2008, core investment grade bonds are yielding almost 5%.

We mentioned last quarter that recessions do not automatically translate to the kind of selloffs we saw during the tech bubble of the early 2000s or the financial crisis of 2008-2009. When the economy went into an eight-month contraction in the early 1990s, the average person on the street may never have noticed considering that less than 2% of the labor force experienced job losses and stocks were positive throughout the entire time. There are many types of recessions and bear markets. A few portfolio managers at JO Hambro recently put this into context with what they termed Small Bear (Ursa Minor), Medium Bear, and Big Bear (Ursa Major). Ursa Minor translates into a monetary tightening bear market. This is on average around a 20% market decline where valuation contractions are the biggest impact to performance. Medium Bears are recessionary driven and average losses are closer to 30%. This is when it is not only valuations, but also profits that take a hit.

Ursa Major is often Bank Crisis driven, and that’s when you get to 50% declines and prolonged market and economic pain. One never knows which experience we will have until after the fact, but there are positives to highlight in that household, corporate, and municipal balance sheets are in a much better place than they were during the financial crisis. The over-levered balance sheets reside with central governments, which, as Japan has shown, can stay burdened for decades with the additional capacity to print money. With that, it appears more likely that we are in Ursa Minor to Ursa territory.

In Q4 2019, ahead of COVID and everything that has come since, we wrote: “We suspect investing in the 2020s will be a wilder ride than in the decade just completed.” We have since written many pieces covering volatility, war, inflation, and interest rates. The underlying melody, although often tweaked, has not changed. We do not encourage emotional reactions to markets, particularly when they are as volatile as they are today. It is important to have a plan, stick with that plan, and make sure you and your advisor are on the same page regarding your goals, timelines, and risk tolerance.

Markets

- For those of us here struggling with inflation numbers, we should at least feel slightly luckier than our friends across the pond (at least those in close proximity to Russia). Our near independence from Russian hydrocarbons is a large reason why our inflation numbers are now less than that of, for example, Germany who just printed 10% YoY price increase. The fact that many of the world’s commodities are priced in USD is another local boon. Case in point, gold is down ~8% this year in USD. It’s up 6% in euros, 12% in pounds, and 15% in yen.

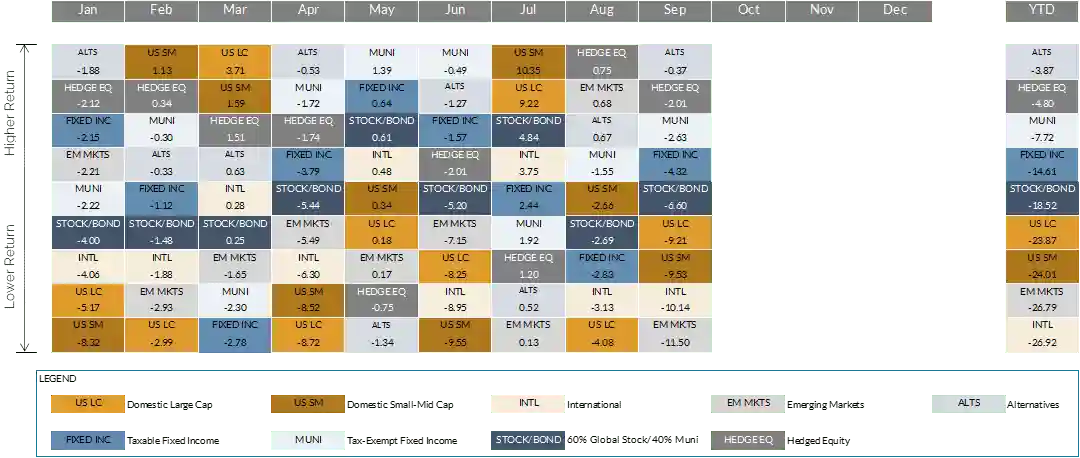

- The equity market had a temporary rebound in July, giving way to weakness into quarter end as markets grappled with hawkish guidance from the Fed. As soon as earnings reporting season ended and there were no fundamentals to anchor to, markets went back to chasing macroeconomic headlines. Taking a back seat to the Fed and inflation but still contributing to volatility were concerns about war, taxes, currency, and geopolitics. Corporate earnings expectations came down slightly during the quarter, but they still reflect positive single-digit expectations for 2022, translating in most of the weakness coming from valuation multiple contraction. Performance is comparable across U.S. market caps, all down in excess of 20% for the year. All but one sector (energy) is down in 2022.

- Overseas stocks were down in local currency terms in Q3 but struggled mightily priced in USD. The USD is now up 17% this year against a basket of major currencies. This is a level not seen since after the bursting of the tech bubble in 2002. An aggressive Fed and global inflation have spurred many central banks (e.g., BOE, ECB) to aggressively raise rates, but the U.S. is in the lead, translating into higher demand for USD not only to purchase aforementioned commodities, but also for the higher yields on offer. Thanks to commodity exports, Brazil is the only major equity market showing positive returns year-to-date not only in local terms, but also in USD (the real strengthened against the USD this year).

- In a reprint of the last two quarters, fixed income, particularly core bonds, have remained under pressure and have not reasserted their status as a safe haven. The more interest rate exposure (aka duration), the greater the penalty. There was a glimmer of positivity in July as the Aggregate Bond Index gained 2.4%, but that quickly reversed course in August and September. As we discussed several times recently, the further yields rise, the better the forward return opportunity becomes and that gives us reason for optimism within our fixed income allocations.

- Alternative investments also had few places to hide during the quarter. Even commodities, which were up big in the first half of the year, sold off in Q3. Strategies with higher net exposures captured the markets downside while strategies that were nimble across asset classes without a directional bias showed better relative performance.