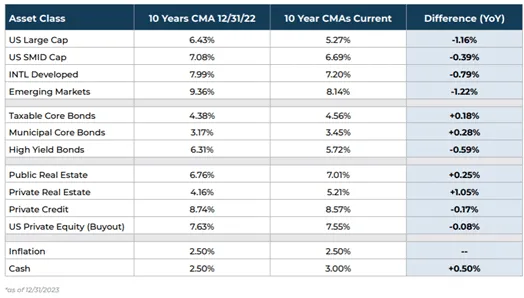

Each year, our Investment Team undertakes a comprehensive review of our capital market assumptions (CMAs) across asset classes. CMAs serve as the foundation of our portfolio construction process because they represent our forecasts for how different asset classes (such as stocks, bonds, real estate, and alternative investments) may perform going forward. The data is then used to approximate the efficient frontier and evaluate tradeoffs between allocating to different types of investments. As part of this process, we conduct a deep review of projected returns, risk, and correlation data from multiple third-party sources, along with our own internal estimates to arrive at a blended, consensus view for each asset class over 10-year and 30-year time horizons.

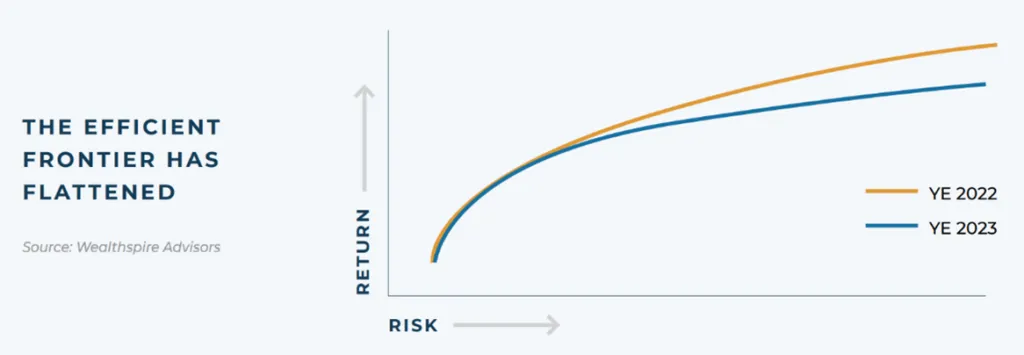

In our recently completed 2024 update, we found that the CMAs point to a significant shift in the tradeoff between risk and return going forward. As interest rates and inflation have moved higher, bond yields (the primary determinant of fixed income returns) have followed suit. At the same time, equity markets have recovered nicely from the bear market experienced in 2022 and have continued to build upon an extended run of strong performance that dates back to the market bottom in 2009. These two undercurrents have combined to compress bond prices and push large cap equity valuations to elevated levels. Higher expected returns for bonds (based on higher yields) and lower expected returns for stocks (based on higher valuations) has led to a flattening of the efficient frontier, which means that the reward for adding incremental risk to a portfolio is much smaller.

10-Year Capital Market Assumptions

30-Year Capital Market Assumptions

Our 2024 Observations

Equities

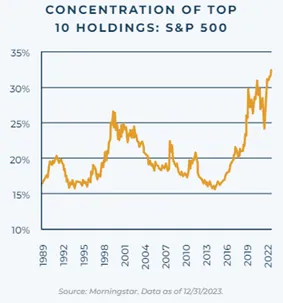

After years of outperformance, U.S. large caps appear expensive relative to history. Valuations are particularly stretched among the “Magnificent 7” tech giants, which now comprise over 30% of the S&P 500 index. This dominance can largely be explained by the explosive growth that these stocks have produced, much of which has been a product of the transformative potential of generative AI. The question going forward becomes whether this momentum can be sustained, and whether the lofty expectations that the market has set for these stocks can be achieved.

The road ahead will be about results, and with the most influential stocks in large cap indices priced for perfection, these names are potentially vulnerable to pullbacks if future results disappoint. We have already seen some of this play out in the first quarter of 2024, with stocks like Tesla and Apple underperforming the broader market after producing stellar returns in 2023.

This backdrop brings valuation back to the forefront, and we believe that investors would be well served to avoid chasing recent returns and look to small/mid-cap and international developed markets for equity opportunities that offer a more favorable entry point.

Broadly speaking, this has also altered the relative value of stocks relative to bonds. As a result of elevated valuations in large cap stocks, the CMAs show a significantly lower return premium for taking equity risk compared to previous cycles. For example, the anticipated return advantage of an aggressive 80/20 stock/bond portfolio over a 55/45 mix has shrunk from 0.74% to just 0.37%.

Fixed Income

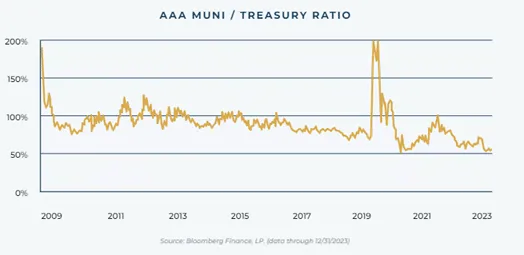

We are also seeing some noteworthy relative value dynamics within fixed income. While higher interest rates have improved the return prospects for core fixed income, municipal bond valuations appear rich based on record-low Muni/Treasury yield ratios. Historically, M/T ratios were consistently high enough that the majority of investors subject to taxation could fund value in adding municipal bonds to their portfolios. However, this is no longer the case. No two investor circumstances are identical, but in the current market, investors should consider that flexible allocations favoring taxable bonds may generate better after-tax outcomes depending upon the investor’s effective tax rate. We view this as just one of many reasons that financial planning is so integral to our wealth management process, and why maximizing after-tax return should be the primary focus of individual investors

Alternatives

Our forecasted returns for alternative assets like private equity, real estate, and credit have exhibited more stability versus public markets. Investors need to be cognizant of the fact that smoother returns in private markets (a common access point for alternative asset classes) are a product of less transparent pricing and not a reflection of lower risk. But with some alternative asset classes expected to produce equity-like returns of 7-8% in addition to portfolio diversification benefits, investors able to take on the illiquidity risks that often accompany these types of investment may stand to benefit over the long term.

Cash

With yields elevated, cash and short-term fixed income have re-emerged as viable asset classes for generating returns above inflation. As price pressures subside toward the Fed’s long-run target range, cash portfolios may offer a rare opportunity to preserve purchasing power while staying defensive. However, investors should be careful not to over-extend into cash, as its short duration nature hinders its ability to produce long-term compound growth.

Looking Ahead

While our 2024 capital market assumptions suggest a more modest return profile for traditional stock/bond portfolios, the re-emergence of cash and fixed income as return drivers provides investors with a wider range of tools to use in portfolio construction. We also believe that actively pursuing diversifying asset classes and opportunistic investments across both public and private markets will be critical in navigating this environment. Our focus remains on building well-constructed, risk-aligned portfolios suitable for the long run and each client’s specific situation.

The full details behind our 2024 capital market assumptions can be found in our annual whitepaper here.

Wealthspire Advisors LLC, Fiducient Advisors LLC, Wealthspire Retirement, LLC dba Wealthspire Retirement Advisory, and certain other affiliates are separately registered investment advisers.

THIS INFORMATION SHOULD NOT BE CONSTRUED AS A RECOMMENDATION, OFFER TO SELL, OR SOLICITATION OF AN OFFER TO BUY A PARTICULAR SECURITY OR INVESTMENT STRATEGY. THE COMMENTARY PROVIDED IS FOR INFORMATIONAL PURPOSES ONLY AND SHOULD NOT BE RELIED UPON FOR ACCOUNTING, LEGAL, OR TAX ADVICE. WHILE THE INFORMATION IS CONSIDERED TO BE RELIABLE, WEALTHSPIRE ADVISORS CANNOT GUARANTEE ITS ACCURACY, COMPLETENESS, OR SUITABILITY FOR ANY PURPOSE, AND MAKES NO WARRANTIES WITH REGARD TO THE RESULTS TO BE OBTAINED FROM ITS USE. IF THE READER CHOOSES TO RELY ON THE INFORMATION, IT IS AT READER’S OWN RISK.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS. DIFFERENT TYPES OF INVESTMENTS INVOLVE VARYING DEGREES OF RISK. THEREFORE, THERE CAN BE NO ASSURANCE THAT THE FUTURE PERFORMANCE OF ANY SPECIFIC INVESTMENT OR INVESTMENT STRATEGY, INCLUDING THE INVESTMENTS AND/OR INVESTMENT STRATEGIES RECOMMENDED AND/OR UNDERTAKEN BY WEALTHSPIRE ADVISORS, WILL BE PROFITABLE, EQUAL ANY CORRESPONDING INDICATED HISTORICAL PERFORMANCE LEVEL(S), BE SUITABLE FOR YOUR PORTFOLIO OR INDIVIDUAL SITUATION, OR PROVE SUCCESSFUL. NO AMOUNT OF PRIOR EXPERIENCE OR SUCCESS SHOULD BE CONSTRUED THAT A CERTAIN LEVEL OF RESULTS OR SATISFACTION WILL BE ACHIEVED IF WEALTHSPIRE ADVISORS IS ENGAGED, OR CONTINUES TO BE ENGAGED, TO PROVIDE INVESTMENT ADVISORY SERVICES. WEALTHSPIRE ADVISORS IS NEITHER A LAW FIRM, NOR A CERTIFIED PUBLIC ACCOUNTING FIRM, AND NO PORTION OF ITS SERVICES SHOULD BE CONSTRUED AS LEGAL OR ACCOUNTING ADVICE. MOREOVER, YOU SHOULD NOT ASSUME THAT ANY DISCUSSION OR INFORMATION CONTAINED IN THIS PRESENTATION SERVES AS THE RECEIPT OF, OR AS A SUBSTITUTE FOR, PERSONALIZED INVESTMENT ADVICE FROM WEALTHSPIRE ADVISORS. A COPY OF OUR CURRENT WRITTEN DISCLOSURE BROCHURE DISCUSSING OUR ADVISORY SERVICES AND FEES IS AVAILABLE UPON REQUEST OR AT WWW.WEALTHSPIRE.COM. THE SCOPE OF THE SERVICES TO BE PROVIDED DEPENDS UPON THE NEEDS AND REQUESTS OF THE CLIENT AND THE TERMS OF THE ENGAGEMENT.

ADDITIONAL CAPITAL MARKET ASSUMPTIONS DISCLOSURES: NOTE THAT THESE ASSET CLASS ASSUMPTIONS ARE PASSIVE, AND DO NOT CONSIDER THE IMPACT OF ACTIVE MANAGEMENT. GIVEN THE COMPLEX RISK-REWARD TRADE-OFFS INVOLVED, WE ADVISE CLIENTS TO RELY ON THEIR OWN JUDGMENT AS WELL AS QUANTITATIVE OPTIMIZATION APPROACHES IN SETTING STRATEGIC ALLOCATIONS TO ALL THE ASSET CLASSES AND STRATEGIES. REFERENCES TO FUTURE RETURNS ARE NOT PROMISES OR EVEN ESTIMATES OF ACTUAL RETURNS A CLIENT PORTFOLIO MAY ACHIEVE. ASSUMPTIONS, OPINIONS, AND ESTIMATES ARE PROVIDED FOR ILLUSTRATIVE PURPOSES ONLY. THEY SHOULD NOT BE RELIED UPON AS RECOMMENDATIONS TO BUY OR SELL SECURITIES. FORECASTS OF FINANCIAL MARKET TRENDS THAT ARE BASED ON CURRENT MARKET CONDITIONS CONSTITUTE OUR JUDGMENT AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. THE OUTPUTS OF THE ASSUMPTIONS ARE PROVIDED FOR ILLUSTRATION PURPOSES ONLY AND ARE SUBJECT TO SIGNIFICANT LIMITATIONS. “EXPECTED” RETURN ESTIMATES ARE SUBJECT TO UNCERTAINTY AND ERROR. EXPECTED RETURNS FOR EACH ASSET CLASS CAN BE CONDITIONAL ON ECONOMIC SCENARIOS; IN THE EVENT A PARTICULAR SCENARIO COMES TO PASS, ACTUAL RETURNS COULD BE SIGNIFICANTLY HIGHER OR LOWER THAN FORECASTED. BECAUSE OF THE INHERENT LIMITATIONS OF ALL MODELS, POTENTIAL INVESTORS SHOULD NOT RELY EXCLUSIVELY ON THE MODEL WHEN MAKING AN INVESTMENT DECISION. THE MODEL CANNOT ACCOUNT FOR THE IMPACT THAT ECONOMIC, MARKET, AND OTHER FACTORS MAY HAVE ON THE IMPLEMENTATION AND ONGOING MANAGEMENT OF AN ACTUAL INVESTMENT PORTFOLIO. UNLIKE ACTUAL PORTFOLIO OUTCOMES, THE MODEL OUTCOMES DO NOT REFLECT ACTUAL TRADING, LIQUIDITY CONSTRAINTS, FEES, EXPENSES, TAXES AND OTHER FACTORS THAT COULD IMPACT FUTURE RETURNS. ASSET ALLOCATION/DIVERSIFICATION DOES NOT GUARANTEE INVESTMENT RETURNS AND DOES NOT ELIMINATE THE RISK OF LOSS.